What’s new in wealth management?

All the news that’s fit to print from global wealth solutions.

|

As we close out the remainder of 2022, there is very little doubt this will be a year for the financial history books. As we stated in our December 2021 update, the S&P 500 was “out of bounds” and needed a correction in price and time. At GWS, we have been calling for a normalization to bond yields for several years, but had no idea the velocity of the move that would ensue.

The 10-Year Treasury yield began 2022 at 1.63%*, after having a low in 2020 at 0.52%. Today, as of 11/18/22, the yield is 3.829%. The yield has increased 148.03%. This is the largest increase in yield recorded since data going back to 1963. However, what is of most concern to investors is the 2-Year Treasury has a yield of 4.531%, an inverted yield of -0.71%. What is the significance of this inversion? The 10-year is controlled mostly by investors and the 2-year by the Federal Reserve interest rate hikes, and very often is a signal that a recession is on the horizon. For the first time in nearly two decades, we can now offer short-term Treasury bonds to investors currently yielding over 4%, subject to change. If you have over 100,000 account and would like to know more, please reach out for a discussion. With inflation over 2% and the job market strong, it puts the Federal Reserve in a tough spot. They are mandated to drop inflation even if a recession is the result. We have been arguing that all the monetary stimulus from the FED and the government during Covid, would result in problems for the financial system. We felt it was just a matter of time; the bubbles in crypto, the stock market, bond market and real estate would eventually start popping. How many times in your life have you seen housing prices rise by double-digit percentage points in just a few years? Only when monetary policy is too friendly. At some point, the party has to end. What does all this mean for investors? While the stock market can ebb and flow in the short term, it’s true colors are revealed over time. For next year, it would make sense there could be a buying opportunity that could potentially present itself. There are many unknowns, such as how high will the Federal Reserve raise interest rates? Will the lagging effects of the unusually high interest rate hikes present themselves as damaging the economy, resulting in a recession? If so, will the recession be mild or deep? Historically, the stock market does not fare well in a stagflation environment. If inflation falls to the 3-5% range, it still keeps investors unwilling to “pay up” for stocks, like they have over the past few years. With that said, the bond market has become more attractive from a yield perspective and may deserve attention. High quality dividend paying stocks could prove to be an attractive investment while the market grapples with these issues. Through the end of the year, historically the stock market looks past all the issues and likes to put on a show. We will see if that is the case this year, but the bottom line for us is that until the Federal Reserve makes clear they are done raising rates, the stock market is going to ebb and flow and be very difficult to navigate. *- https://www.macrotrends.net/2016/10-year-treasury-bond-rate-yield-chart

0 Comments

As summer begins to wind down, we feel it is a good time to provide some thoughts on the

financial markets. There has no doubt been a lot of information to digest since the start of the year. The best way to understand the state of things is to steal the phrase from an old Clint Eastwood movie: We are all dealing with “THE GOOD, THE BAD and THE UGLY.” We’ll take a few minutes to discuss each of these, but at the end of the day, it’s anyone’s guess as to what happens from here. Literally both the stock and bond markets could be 10% to 20% higher or lower from here. Much depends on reading the Ti leaves of the Federal Reserve. Will they continue to withdraw monetary stimulus, creating tight money; will they continue to raise rates into a slowing economy; or will they eventually pivot and do the opposite? The answer to these questions could actually be the difference between a large gap between where the markets stand today, S&P 500 4100, or 10%-20% higher/lower. First, THE GOOD…

Second, THE BAD…

Third, THE UGLY…

Since the Great Financial Crisis of 2008/2009, the Federal Reserve has been mostly loose with its monetary policy measures. This has acted as a backstop to the financial markets and kept investors singing its praises. What we don’t know is whether inflation will react to Federal Reserve actions over the past six months. Will inflation peak and begin to fall once disruptions from Covid 19 shutdowns and supply-chain bottlenecks begin to ease? Will the stock market look past some of these issues and see brighter skies ahead? Often the market defies logic, tends to see past issues, looks to the future rather than the now. We see this time and again, but will this time be different? Here is the message for investors. If you can look past all the noise, invest for the future, three to five out, with some of your portfolio, then this may be a good opportunity. Presently, to get back to the highs for the year, the S&P 500 would need to climb approximately 16%. If you feel it’s a good risk/reward, give us a call. Take a few minutes to complete our online risk profile assessment. With all that is taking place, we cannot say with any certainty what will happen for the rest of the year, we don’t have a crystal ball. We can guide investors where we think the probable sectors or funds of the market could be if one feels inclined to add stock-market exposure. That’s a truly interesting topic if you’re so inclined to have the discussion. Thank you for taking the time to read our thoughts… Mike Reinhart & Leonard Rhoades You can access our online risk profile assessment by going to: www.GlobalWealthSolutionsLLC.com and clicking on the tab entitled, (Risk Assessment Quiz) 1. shorturl.at/ehR08 2. shorturl.at/hlvxY 3. shorturl.at/fovX8 Nearly halfway through 2022 and what we can say for certain … markets have been on a roller coaster ride. The trio reflected in the title of this blog post has rattled investors year to date. Reality is that since last Fall, many stocks within the Nasdaq and S&P 500 are down double-digit percentages. Cathy Woods’ ARK Innovation ETF, symbol ARKK1, that gained so much attention during the COVID-19 Pandemic, is down over 50% year to date. The bond market measured by the Aggregate Bond Index2 is down over -10% YTD, while the S&P 5003 is negative by just over -13%. Truly, this is one of the most complex times in the markets … a time that we’ve been anticipating for several years. When would stocks and bonds both deliver potential negative returns? It doesn’t happen very often, but with interest rates historically low and inflation historically elevated, it makes for a recipe for volatility. Aggregate Bond Index Chart – Since 200  There have been very few places to hide from the volatility, and add to it the war between Ukraine and Russia. An example? A 60 stocks/40 bond moderate portfolio,4 offered by many financial firms, is down over -10% this year. The good news, the FED is hiking interest rates. For conservative investors, that should give us an opportunity in the coming months to get higher rates on money market and short-term bonds. The chart above reflects the price of the aggregate bond index. Rising interest rates results in falling prices, levels not seen since early 2000s. In addition, as we’ve written about over the past month or two, it’s our humble opinion there could be a better opportunity to invest in high quality stocks once the market digests the rate hikes and inflation. We also need to see how high inflation, the war in Ukraine and rate hikes affect corporate earnings. Our December 23, 2021, blog post discussed how the S&P 500 was “out of bounds” and would need a rest, at the very least. The chart below highlights an area of support, which gets the markets back into a more reasonable pattern. We will see if over time that becomes a reality or not. S&P 500 Index Chart – Since 2000  The financial markets have been largely “buoyed” by the Fed’s “easy money” corporate buybacks, low interest rates, and five mega cap technology stocks. The Federal Reserve, as of this month, are taking away the punch bowl. Not only have they started a rate hike cycle, but we’ve also entered “QT” (quantitative tightening).

What is QT? Simply think of this as the opposite of what they’ve done for emergency purposes, such as during the 2008 financial crisis and the 2020 Covid pandemic crisis: Liquidity for the financial markets and bond purchases to drive down interest rates, hoping to spur economic growth. The questions throughout the years have been…

The answer to those questions appears to be playing out, but will likely take more time to understand the aftershocks. Corporate executives such as Jamie Dimon of JPMorgan recently made surprising statements. In fact, Mr. Dimon stated that we could potentially find ourselves in a financial hurricane.6 Bottom line is, it’s a bit of a guess by everyone. It’s hard to know what the Federal Reserve will ultimately do with interest rates, how the economy will be affected by less “juice” from the Fed, and what the financial markets have discounted thus far. There was an Interesting interview by former president of the Federal Reserve Bank of New York. You can access it by googling “If stocks don’t fall, the Fed needs to force them”6 – Bloomberg. Happy Summer! Mike Reinhart and Leonard Rhoades Source:

Hello, and welcome to 2022! This year has thus far proved to be an eye opener for Covid and the financial markets. December 23, 2021, we wrote an article that laid out our 2022 financial thoughts. Three major themes were highlighted:

The fact of the matter is, unless you can read the minds of the Federal Reserve, no one on earth other than that committee knows what will prompt them to raise interest rates for the first time in over two years or how the market will react. What we do know is that since the 2008/2009 financial crisis, along with the Covid-19 crisis, the Federal Reserve seems to dictate where the stock market goes.  For several years, all eyes were on the stock market, watching it climb. As usually happens at levels that get over-extended, retail investors want to chase the market higher. Fear of missing out drives emotions until the market begins to correct, and then the other side of the emotional roller coaster overrides and selling pressure escalates. While the stock market generally takes the stairs up, the elevator down, and then waffles back and forth for a while, overall, much of it will depend on the Federal Reserve. The financial news media will take either side and make things sound better or worse than what they truly are. I!ve listened intently to the rhetoric over the past few weeks. It has turned from extreme favor to negativity in that short window of time. Companies’ values in the past was a gauge for the market; was it expensive or was it cheap. As mentioned, today, and for the past 13-14 years, the Federal Reserve has been the measure of the market. If they stay with "easy money,” the stock market has risen. Once the punch bowl is talked about being pulled, the stock market gets grumpy. Should the market reach that 20% milestone, if you!re willing to take some stock risk to your portfolio, it might be a spot to add some exposure. With interest rates being as low as they are currently, and with the threat of interest rates rising, the bond market overall appears it may have back-to-back years of losses...unless something changes. As we!ve stated, please take the time - only about 3-5 minutes - to fill out our risk profile questionnaire. You can access it by visiting our website, www.GlobalWealthSolutionsLLC.com, and then clicking on the tab titled "risk assessment quiz.” Thank you for reading and we hope you enjoy the remainder of the winter months. "Spring is right around the corner.” Mike Reinhart and Leonard Rhoades  Hello to all and hope everyone enjoys the remainder of 2021. To begin, we want to keep this as short as possible so that everyone takes a moment to read it carefully. While we attempt to talk with everyone several times per year, sometimes it’s just easier to get some important points across in letter format. So please take just a moment to understand our thoughts on things as we move forward into 2022.

With that said, I think everyone believed putting 2020 in the rear-view mirror would be a way of making a fresh start post pandemic. Now I personally find myself thinking the same thoughts about 2021 as we head into 2022. While the Federal Reserve and the Federal Government blasted the economy with an atom bomb that proved to be a financial hero of sorts, it also appears to have created some short-term, and possibly longer-term, aftershocks that may or may not be felt for some years to come. What do I mean? Honestly, I could write a book on this subject, so to keep it within the scope of this letter, I will make a few observations. First, it seems every asset class that exists - from housing, to stocks & bonds; from gold, to land; Bitcoin or ANY type of recreational item - is out of whack based on historical norms. The stock market, measured by the Shiller PE (price to earnings) Ratio, as of the date of this letter, is just a few points away from its highest measured peak ever. That peak was 44.19 in December 1999; we are currently at 39.29. The mean is 16.90 (https://www.multpl.com/shiller-pe) meaning the stock market would have to drop nearly 60% just to hit it’s historical fair value. While valuation by itself is not a reason to buy or sell stocks, it gets our attention at these levels. In part, this dislocation has been created by historically-low interest rates and extreme monetary policy action. Looking under the hood of the major indices, it appears once again 6-7 stocks make up most of the gains, and many stocks have fallen 10%-20% or more since February of 2021. This should be alarming if that handful of stocks break down. What would happen to the overall market? While stock valuations seem high, the momentum of the market has continued and until it stops, it’s anyone’s guess how high it will go. However, one would think some time within the next year, there should be a reversion to the mean. Since the pandemic lows in March 2020, the stock market has gone parabolic, and as such, it is unlikely to be able to continue on that trajectory. Something, at some point, must give and produce a reversion to the mean. Could the stock market go higher from here? Certainly! However, as we’ve experienced in the past 20 years, at some point, things get just too lopsided. Looking at the chart of the SP 500, the rally is technically out of bounds. While we favor stocks for the long run, there could certainly be some turbulence in the next year or so, which continues to keep conservative investors cautious. If you have a long-term time horizon and are ok with market volatility, then over time, we would think history should continue to be on your side. The questions will be surrounding the Federal Reserve, will they be able to raise interest rates in 2022? How will this affect investors’ willingness to pay up for stocks? What ripple effects will we see as a result? What about bonds? This is generally the area of investment for more conservative investors. This, too, has been a challenge. For the most part, the bond market has experienced a negative return for 2021. Interest rates are at extreme low levels. Debt, too, is at an all-time high, the United States debt is over 29 trillion (https://www.usdebtclock.org/). With interest rates so low, it’s difficult to generate a total return for investors. Many have thrown in the towel and scrambled to buy stocks. Generally, we see this as a capitulation of sorts that is often a sign of a top in stocks. There are lots of questions going in to 2022. Will the pandemic turn into an endemic? While seasonality is generally favorable at year’s end, will volatility increase the first half of 2022 and bring valuations to a more reasonable level? That could prove to be a marker of sorts to get more involved in the stock market; however, with the Fed reducing its bond purchases and hinting to raise rates, inflation readings are the highest they’ve been since the late ‘70s & ‘80s, which is now triggering inflation. Asset prices have increased, commodity prices have soared and there have been supply chain issues due to the pandemic. Due mostly in part to technology advances, inflation has been at bay for the better part of 20 years. We’ve had spikes from time to time, but all in all, inflation has been subdued. In 2008, the price of a gallon of gas was about what it is today, 13 years later. Commodity prices have soared over the past year, albeit from low levels. The pandemic has created supply disruptions, yet when we get past the pandemic, these should level off and reduce inflation levels… hopefully. Bottom line, there is a lot going on in the financial markets. There is no perfect asset class or product that can be an end-all solution. In my opinion, having a diversified portfolio over time is the tried-and-true method of investing. It’s not all doom and gloom. Profits are robust and companies appear to be doing well in America. Like most of us, we want to be able to make money and don’t want to risk too much. Certainly, we are in challenging times that are difficult to navigate. Just buying the stock market and holding has proved well for several years, but at some point, looking away and holding your nose could prove detrimental. The stock market takes the stairs up and the elevator down during times of exuberance. We urge you to fill out our risk profile if you haven’t already. We mention it often, either in conversation or through updates like this. Please visit www.GlobalWealthSolutionsLLC.com and click on the risk assessment quiz tab. It’s a five-minute exercise that helps us help you. How much risk should I be willing to take? That is the question many investors ask themselves, especially when the stock market seems to climb unabated day after day.

Reality is, it’s up to the investor. If you were to put money into an individual stock, you run the risk of losing the full investment. If you put the same amount into a mutual fund, due to the broad diversification of stocks in the pool, you can still lose money but not likely the full amount invested. A good place to begin the decision as to how much risk to take, is to complete a risk profile assessment. This helps by asking questions to see what your level of risk is. Should you invest 10%, 20%, 30% or more in stock mutual funds? The assessment will help assist with your decision. If an investor were to put 20% into stock mutual funds and the stock market dropped 15%, how much would you possibly lose during that time frame? Let’s do the math. Assume you had a portfolio worth $500,000. If you had invested 20% in a stock mutual fund that dropped 15%, your $100,000 (20%) allocation in the mutual fund would be down $15,000. Could you stomach that amount? It’s possible the amount invested in bond mutual funds, the other 80%, would increase in value and/or pay interest to help offset the decline. With that said as we are all aware, there is risk in investing. The amount of risk someone is willing to take is up to the individual, not the financial advisor. Interest rates are at historical low levels. Consider the levels below for the 10-year treasury, the proxy for interest rates. 10-Year treasury yield calendar year starting yield.1 -1990 7.94% -2000 6.58% -2005 4.23% -2010 3.85% -2015 2.12% -2019 2.66% -2020 1.88% -2021 0.93% Conservative investors that do not want to take the risk of the stock market have seen interest rates fall to levels never seen in the history of the financial markets. If you are a conservative investor, then it has been a challenging environment to generate a total return in today’s environment. Do you own a certificate of deposit, bank savings or checking account? If you do, then you no doubt get a good laugh at the interest deposited each month. To reiterate the purpose of this information…take the time to complete a risk profile assessment to see if you could allocate some of your account to stock mutual funds. Give thought to how much volatility you are willing to take within your portfolio. No one can successfully forecast the next major correction. Corrections of 10%-15% are normal within the context of the stock market. If you’re willing to add some exposure to additional risk, you must take the step of filling out the risk assessment and communicating your willingness to your financial advisor. You can access our online risk profile assessment by going to: www.GlobalWealthSolutionsLLC.com and clicking on the tab entitled, (Risk Assessment Quiz) 1-https://www.macrotrends.net/2016/10-year-treasury-bond-rate-yield-chart Hello,

Hope you’re enjoying the remaining days of summer with family and friends. We wanted to take a moment to explain a few items of interest regarding the financial markets, interest rates and risk profile assessment. As many of you may know, the Federal Reserve has kept interest rates at emergency levels since the Global Pandemic began in the early Spring of 2020. Prior to that, since the Great Recession of 2008/2009, interest rates for most of that time were extremely low compared to historical averages. This has made it a very challenging investment landscape for those seeking a total return with low to moderate risk. If you were to make some comparisons…check your bank CD rates or your checking account interest. These are likely yielding roughly .10% compared to the 10-year treasury yielding just below 1.50%. To put this in perspective, the 10-year treasury was yielding 4.50%-5.50% just prior to the 2008/2009 Great Recession. These are challenging times for low-risk investors. What about the stock market? This area of the financial market too appears fueled by low interest rates, “easy money” as some may refer to it. The current price to earnings ratio of the S&P 500 is roughly 28 times earnings. To put this in perspective, since 1871, the average valuation is 14.6 times earnings. For a more recent historical average, 1990, the valuation stood at 14.2 times earnings. By 2000, 15.5 times earnings…2010, fair value rose to 17.8 times earnings. Last year, 2020, earnings hit 19.7 times earnings. An excerpt from James Paulsen, Chief Investment Officer with The Leuthold Group most recent newsletter stated the following: “From 1990-forward, however, the average valuation of the stock market has been persistently climbing. As a result, for the entire time from 2000-to-present, the 30-year-average P/E ratio has been above the old valuation range. Furthermore, the trailing 30-year-average P/E multiple of 20.2x is more than 30% above the highest valuation ever reached between 1871-1989! Clearly, for reasons beyond the scope of this note, during the last three decades, the U.S. stock market has established a new and much higher valuation range. Could it eventually return to the confines of the 150-year average? Absolutely. Will that likely happen any time soon? Probably not.” Without question the stock market continues to adjust the valuation investors are willing to pay. Earning thus far have continued to benefit from low interest rates, easy money from the Federal Reserve and company buybacks. Will this continue and if so for how long? The answer to that question is difficult. Additional questions come to mind that will likely determine the direction of the stock market, at least in part. Will the Federal Reserve continue easy money policy? Will the Global Pandemic persist with additional strains that continue to create pauses in the economic recovery? With all this stated, if you would like to add stock market exposure to your portfolio, please let us know. In addition, take just a few moments and complete the online questionnaire that will help to determine your tolerance for stock market risk. It can be found by going to: www.GlobalWealthsolutionsLLC.com and then go to the “risk assessment quiz” tab. SOURCE: https://advisors.leutholdgroup.com/research/paulsen/2021/07/30/what-is-the-sp-500s-normal-pe-multiple-202x-trailing-eps.23081 In our first article in the series, “Would you like to retire early,” we discussed the bond market. In my opinion, this is potentially one of the biggest hurdles investors will need to grapple with over the coming years. Debt throughout the world has risen to stunning levels. Just look at www.usdebtclock.org. The US debt is alarming! This has a potential of becoming an issue at some point in the future; in particular, for our children or grandchildren.

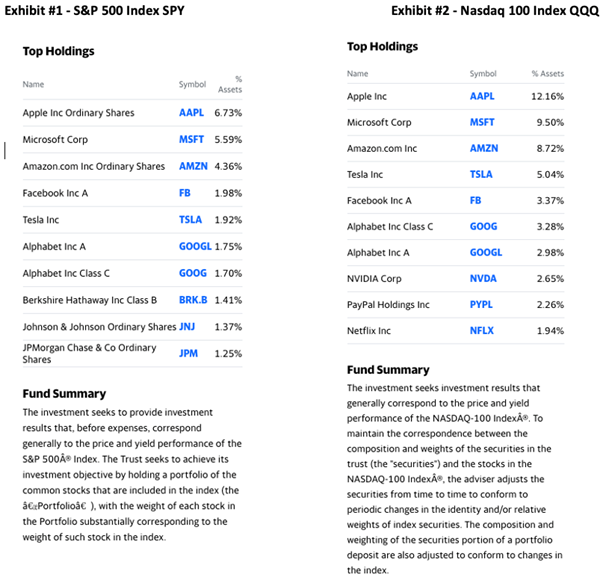

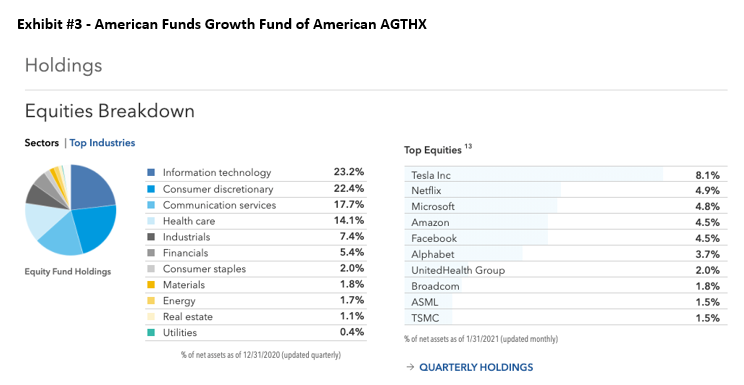

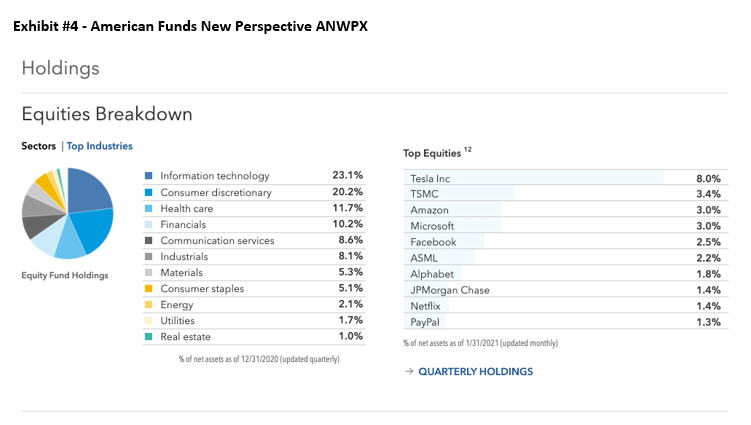

As inflation becomes more of a concern, along with increased government spending, interest rates tend to rise. To reiterate our previous post: As interest rates rise, the price of the bond mutual fund falls in value. Depending on the duration of the bond fund, along with the type, this could have a long-term effect on a portfolio such as a moderate allocation, where 40%-50% is invested generally in bond mutual funds. There are few options that have been discovered that achieve historically what the bond market has been able to accomplish. Most investors view the bond market as “the safe market,” but the reality is there is no safety in any “at risk” investments. Investors buy bonds in an attempt to provide interest and stability to their portfolio. That so-called stability is hard to achieve with the potential of rising rates, or just simply stubbornly low interest rates. What are some alternatives? An option is a certificate of deposit, which, of course, with interest rates where they are, there is relative safety, but the tradeoff is low returns. The risk of principal being lost is alleviated, but there is still truly little hope of return other than what is stated. Could there be another option that could achieve the same level of protection investors want, and at the same time, the potential for moderate returns? The fixed index annuity is an option that is discussed in my book, The Informed Retiree. Why do we consider this an option? Again, if the desire is to protect principal and provide moderate returns, then the fixed index annuity has been a viable candidate. Yet even more benefits could be achieved. We feel this annuity type, which has been around since the mid 90’s, can do even more heavy lifting within a portfolio. We will talk about this in our next post. Stay tuned! If you would like to read my book, The Informed Retiree, visit my website www.TheInformedRetiree.com or send me an email to [email protected] Also available on Amazon.com Advisory services offered through J.W. Cole Advisors, Inc. (JWCA). Global Wealth Solutions and JWCA are unaffiliated entities Over the past few years, technology stocks have outperformed other broad market indices. This is due to a number of reasons, one being the decline of interest rates, as we’ve discussed in prior articles. Low interest rates tend to increase interest in growth stocks over value-oriented stocks. One thing to note is that could eventually change if interest rates were to begin to rise over time back to normalized levels, and especially if the Federal Reserve were to increase rates in the future. See my book chapter 5 on the bond market. With that said, one item of interest to note is the correlation between the index funds, mutual funds, and the “market weighted” S&P 500 Index. What do I mean by “market weighted”? The S&P 500 Index that we all see on CNBC or The Nightly News is an index that invests a percentage of its holdings in each of the 500 companies based on their market capitalization (the value of the company). A heavier weighting is assigned to stocks with higher value. See Exhibit #1. Just over 24% of the value of the index is invested in six companies that are in the technology sector. Exhibit #2 lists the Nasdaq 100 stocks, and the top stocks are nearly a mirror image of the S&P 500 Index, weightings slightly different, but the same companies listed at the top. What does this all mean? First off, the S&P 500 index has benefited over the past several years from the growth of the top technology stocks like Apple, Google, Microsoft and Amazon. We would think that the performance has been slightly skewed with a nearly 24% allocation to so few stocks in one sector.  Then of course we have some of the top performing mutual funds that also invest a large portion of their portfolio to these stocks. Afterall, a mutual fund’s performance needs to keep up with the index in order for individual investors to use their fund or fund family. American Funds, for instance, are used by many of the well-known financial companies that invest for individual investors and 401k plans. This is simply an example to show how first, you can overlap holdings just by simply buying two mutual funds from the same family of funds. Second, you may own many of the same holdings if you own other fund families as well, including the S&P 500 Index Fund offered by Vanguard. It’s important to dissect your stock holdings within the mutual fund or other financial products in order to make sure you aren’t just duplicating holdings. See Exhibits #3 and #4.   What do you do if you’re unsure about having too much exposure to technology stocks or just would like to know if you’re diversified enough? It’s always a good idea to understand your portfolio, to know whether you’ve leaned too much in a certain sector. Should technology stocks become out of favor over the coming years due to a change in the investing landscape, or just need to rest for a while, many of the mutual funds that have done very well may suffer.

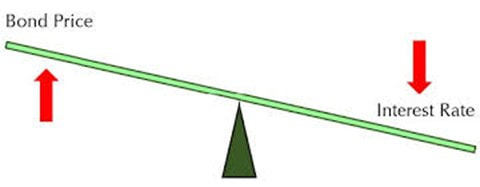

It’s wise to take the opportunity while the subject is on your mind and get a second opinion. Whether with us or someone else, it’s wise not to take for granted changes in the investing environment. When investors change their mindset, what once worked for many years can change quickly. The pendulum can swing and take years to get back to equilibrium. Sometimes investors that have stuck with a certain mutual fund for years cannot understand why it no longer delivers the returns they were accustomed to. This can be due to individual holdings, as we’ve discovered, or due to the fund owning bonds in addition to stocks, and the bond market loses at the same time the stock market loses. Not something investors have been accustomed to in a very long time. Another mistake that is often made with investors is they look for last year’s winners and buy them, as they believe that win streak will continue. That can certainly work some of the time, but it’s not an investment plan of action that should be counted on to work consistently. Everything stated above is meant to bring to light that there is a need to look under the hood of your portfolio holdings. Just having a list of mutual funds on your statement does not necessarily mean you’re diversified, or that those funds are not highly correlated. Please take the time to analyze your portfolio. We’d be happy to start with a no-obligation “strategy session.” Send me an email or phone call. You can also schedule time on my calendar by clicking here. If you would like to read my book, The Informed Retiree, visit my website www.TheInformedRetiree.com or send me an email to [email protected] Also available on Amazon.com Advisory services offered through J.W. Cole Advisors, Inc. (JWCA). Global Wealth Solutions and JWCA are unaffiliated entities Over the years, I have had the conversation with many pre-retirees who ask the question, “What do I need to do to retire early?” The answer is not just one thing will do; it takes a series of strategic moves to be comfortable with the decision. Why do we say this? People are living longer than they did in the past, which means our money and income needs to last as well. In addition, we have a good chance of using a portion of our assets towards assisted living or nursing care. We could save a large nest egg, only to experience a sideways or declining market drop, one similar to 2000-2009. When we retire, as it relates to stock market, valuations and interest rate levels can also have an effect. How our portfolio is diversified and if we have a steady stream of income not dependent on the stock or bond markets is yet another factor. These and many more questions will be discussed in the series, “Would you like to retire early?” We will begin with the topic of diversification.  Many of the name brand firms in the financial services industry use diversification to assist in reducing volatility and proving an overall total return. Harry Markowitz in the 1950s pioneered modern portfolio theory 1*. The idea of dividing a portfolio into a basket of different size companies with differing objectives, international, real estate, commodities, and bonds, was a way to reduce overall risk. Many of the firms on Wall Street still utilize this approach. At first glance, it still seems to make good sense; however, there are, in my opinion, a few flaws that could be improved upon. One of the biggest flaws I currently see is the portion allocated to bonds. Over the past 40 years, interest rates have fallen from the high teens to sub 1% in the 10-year Treasury 2*. If you do not understand how interest rates work, think of a teeter-totter. As rates fall, think one side of the teeter-totter, the other side goes up, which in this illustration, is the price of the bond. Simply put, interest rates have fallen to levels never seen in the history of the bond market, and as such, the value of the bonds have risen accordingly. If you would like to learn more, read chapter 5 of my book, “The Informed Retiree.” It can be found at www.TheInformedRetiree.com  With that said, bonds just do not provide enough horsepower any longer to enhance total return for a portfolio, nor do they provide enough of a cushion to offset stock declines for more conservative investors. So, all in all, the once powerful diversification into bonds may have run its course, and thus lost its luster. However, it could be worse than we might expect. What if rates actually began to rise over the coming years? What would happen? Think of the teeter-totter illustration again. If rates rise rather than fall, as they have for decades, then the opposite happens, price of the bond loses value.

This phenomenon would have a bigger impact on bond mutual funds than individual bonds. Why? Individual bonds eventually have a maturity date; thus, the investor receives their investment back as long as the company fulfills its obligation. Yet mutual funds do not have a maturity date; they are a perpetual investment, and thus continue to follow the trend of underlying interest rates - and here is the point - whether they go up or down 3*. Understand, not all bonds are equally affected by interest rates. There are other factors that may affect the value of a bond beyond just interest rates alone. However, for the most part, interest rates drive much of the underlying performance of the bond market. What are investors to do? Look for future articles in this series to read about the potential solutions to the problem that could exist for many years. If you would like to read my book, The Informed Retiree, visit my website www.TheInformedRetiree.com or send me an email to [email protected] Also available on Amazon.com Advisory services offered through J.W. Cole Advisors, Inc. (JWCA). Global Wealth Solutions and JWCA are unaffiliated entities |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

November 2022

Categories |

RSS Feed

RSS Feed